Payments Are Not Enough : Insights from Nigeria's Fintech Evolution

Rotimi Owolabi

Rotimi Owolabi

Key Highlights

- Payments Have Scaled, but Economic Participation Extends Beyond Transactions: Nigeria’s adoption of digital payments has increased rapidly, but economic participation is shaped by access to credit and capital rather than transaction activity alone.

- The Constraint Has Shifted Beyond Payment Access: As payment adoption has expanded, challenges now lie in infrastructure gaps, regulatory constraints, and limited financial intermediation.

- Payments Leadership Is a Starting Point, Not the Outcome: Nigeria’s mature payments infrastructure provides a strong foundation, but economic impact depends on deepening access to credit and capital.

Nigeria's fintech success story is undeniable. With over 11 billion transactions processed in 2024, up from 5 billion in 2022, the country has risen to be a continental leader in electronic payments adoption. When focused on the adoption metrics, these numbers paint an impressive picture. Yet, the adoption metrics obscure a more complex reality, as access to electronic payments does not on its own translate to economic empowerment.

The Central Bank of Nigeria's 2025 Fintech Report reveals that 26% of Nigerian adults remain financially excluded despite the proliferation of digital payment platforms, with exclusion rates reaching 37% in rural areas and 47% in the North. The coexistence of high transaction volumes and persistent exclusion reflects a distinction between access to digital payments and access to the financial tools required for productive economic participation.

The distinction matters because economic development requires more than the ability to send and receive money. True financial inclusion demands access to credit for business expansion, savings mechanisms for wealth accumulation, and insurance products for risk management. While Nigeria's payments infrastructure has democratized transactions, it has not yet democratized capital formation, which is the essential driver of entrepreneurship, employment, and upward mobility.

Mature Payments Infrastructure, Shallow Financial Deepening

The Nigeria Inter-Bank Settlement System (NIBSS), Nigeria’s payment infrastructure launched in 2011 created a strong foundation for digital finance. The NIBSS Instant Payment (NIP) platform now ranks among the world's most mature payment systems, hitting an all-time high of N1.07 quadrillion in December 2024. This achievement merits wider international recognition and positions Nigeria as a reference point for emerging markets.

However, the same infrastructure that enables seamless payments has not translated into access to credit and capital. Payment Service Banks, despite their extensive agent networks and low-cost account offerings, face regulatory restrictions that prohibit lending.

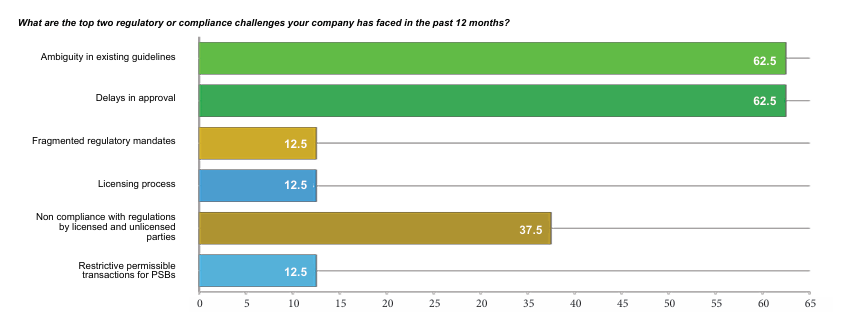

Survey evidence from the CBN 2025 Fintech Report also highlights compliance as a system-level bottleneck. With about 87.5% of surveyed firms indicating that meeting regulatory and risk requirements materially impacts their innovation capacity.

Stakeholders from the report consistently identified digital identity integration as a constraint. The challenge is not the absence of identity systems like the BVN and NIN, but their fragmentation, integration gaps and uneven performance across existing platforms as major barriers to reaching excluded populations. Without reliable identity verification, fintechs struggle to extend credit to informal enterprises and unbanked individuals, precisely the segments where financial intermediation could have the greatest economic impact.

Similarly, the incomplete rollout of interoperability frameworks like the Global Standing Instruction (GSI) limits credit ecosystem development. While GSI was designed to enable seamless loan repayment collection across institutions, its expansion to fintech lenders and microfinance banks remains incomplete. This increases credit risk for non-bank lenders, raising borrowing costs and reducing credit availability for MSMEs and low-income borrowers.

Access to Payments Are not Enough

The economic case for moving beyond transaction inclusion becomes clear when examining the constraints faced by Nigeria's informal economy, which employs about 76% of the Nigerian workforce. Informal enterprises and MSMEs lack access to formal credit not because they cannot make payments, as many actively use mobile money and digital wallets, but because the financial system lacks the data infrastructure, risk assessment tools, and regulatory frameworks to safely extend credit to them.

While Nigeria's fintech ecosystem has optimized transaction efficiency by reducing friction, lowering transaction costs, and expanding reach, optimizing transactions alone cannot address the barriers to access to credit and capital. There remain constraints around the absence of credit histories, limited collateral, information asymmetries between borrowers and lenders, and regulatory frameworks designed for traditional banking rather than inclusive digital lending.

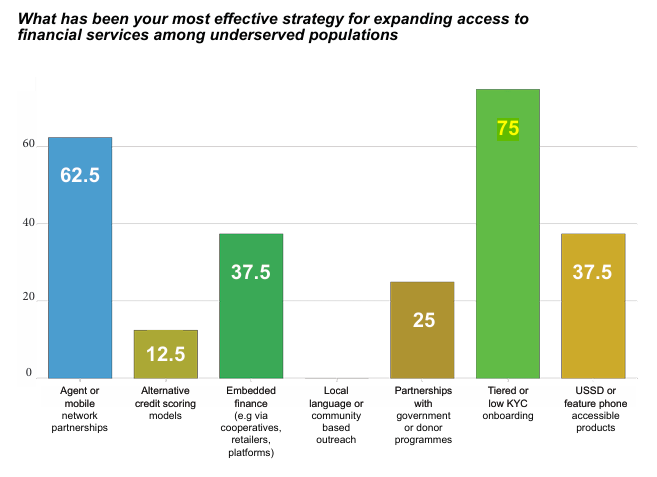

The stakeholder feedback in the CBN report underscores this tension. While 75% of fintech respondents identified 'tiered or low-KYC onboarding' as their most effective financial inclusion strategy, the inability to lend remains a constraint particularly for Payment Service Banks (PSBs) which are run by telcos and have a stronger reach in underserved regions.

A Strategic Shift Toward Productive Financial Inclusion

Moving beyond transaction inclusion requires a deliberate strategic shift across three dimensions: infrastructure evolution, regulatory modernization, and ecosystem incentive alignment.

-

Infrastructure Evolution: Digital identity systems must transition from verification tools to comprehensive credit enablement platforms. This means not only improving BVN and NIN API reliability but also integrating payment transaction data, utility payment histories, and alternative data sources into credit scoring frameworks. India's experience with Aadhaar-linked credit systems and account aggregation frameworks offers relevant lessons for Nigeria's context.

Equally critical is expanding data interoperability beyond payments. The proposed expansion of the Global Standing Instruction to fintech lenders and microfinance institutions would reduce credit risk and lower borrowing costs. Open banking frameworks, through the CBN’s Operational Guidelines for Open Banking (2023), requires accelerated implementation with clear technical standards and consumer protection safeguards. Credit data-sharing systems need both improved accessibility and reciprocal contribution requirements to ensure sustainability.

-

Regulatory Modernization: The regulatory architecture must evolve to enable financial intermediation under appropriate safeguards. This could involve reviewing the PSB lending restrictions, introducing dedicated digital banking licenses with proportionate capital requirements, or creating regulatory sandboxes specifically focused on inclusive credit models.

The CBN 2025 Fintech report highlights strong stakeholder appetite for collaborative policy development: 100% of surveyed fintechs expressed willingness to participate in regulatory pilots, sandboxes, or working groups. This creates an opportunity for co-creation of frameworks that balance regulatory oversight with innovation.

-

Ecosystem Incentive Alignment: Current pricing frameworks, while beneficial for transaction affordability, may inadvertently discourage infrastructure extension to remote or low-income markets. Stakeholders noted that ultra-low transaction fees reduce commercial viability for serving rural populations. Rebalancing inclusion incentives could involve periodic review of interchange rules, introducing tiered pricing or creating explicit subsidies for last-mile infrastructure.

The proposed Fintech Credit Guarantee Window also represents another incentive mechanism. By de-risking MSME lending through blended finance partnerships with development institutions, such a scheme could catalyze credit flow to underserved populations while maintaining commercial sustainability for participating fintechs.

Redefining Success Metrics

Transaction volume, while impressive, is an incomplete measure of financial inclusion's economic impact. As Nigeria's fintech ecosystem matures, success metrics must evolve to capture productive economic participation: credit penetration among MSMEs and informal enterprises, savings accumulation among previously excluded populations, reduction in reliance on expensive informal finance, and ultimately, measurable impacts on entrepreneurship, employment, and income mobility.

The gap between where Nigeria is and where it could be requires recognizing that payments infrastructure, however sophisticated, is a means rather than an end. The end is economic opportunity, wealth creation, and upward mobility for millions of Nigerians.

Author

Rotimi Owolabi

Analyst